The Abolishment of the Pension Lifetime Allowance and how it Impacts my FIRE Plans

The answer may surprise and bore you

The Lifetime Allowance (LTA) is a popular topic for questions over on the /r/fireuk and /r/ukpersonalfinance subreddits as, and rightly so, people are concerned that they may end up “hitting it” and potentially they may not experience any tax advantage in the long run at all. There is a great post on Monevator that discusses the LTA in detail here that I recommend you at least skim.

However, I expect over the next few weeks these questions will change to “how does the abolishment of the LTA impact your retirement plans?”, especially for us FIRE folk.

Today, in quite a surprising turn of events the UK Government scrapped the Pension LTA completely. There was rumours before the budget that they were going to raise it, but to abolish it was not something anyone expected. The high level summary of the relevant changes announced in the budget are:

The Lifetime Pension allowance is going to be scrapped from the 6th April 2023.

The annual pension allowance is going to increase from £40,000 to £60,000 from the 6th April 2023 .

After spending some time reading about it today, doing some modelling in my spreadsheet and bowing to the poster of Jeremy Hunt on my bedroom wall, I thought I’d share with you the changes I am making to my retirement plan which is to make absolutely no changes at all. Here’s why.

#1 I need to access a large chunk of my cash before retirement age

To retire early in line with my plan, I need to be able to drawdown cash from around age 45. At this current time, the earliest I will be able to access my private pension is age 57, and that is if they do not update the pension age again. Just 2 years ago, I would have been able to draw down my pension at age 55, and there are plenty of rumours that the government will update the state pension age to be 68 soon and eventually even 70. This seems likely to me since people are living longer and having less kids; pension costs are going to become unsustainable. If the state pension age raises to 70, they will almost certainly raise the private pension access age to 60 and I need to plan for that. Further supporting evidence for this is the budget’s focus on getting people “back to work”.

Pushing accessibility to pension pots back a couple of years is more stick than the current carrot approach introduced as part of this budget, but it will ensure that people do work longer.

#2 I believe this was mostly a short term political play

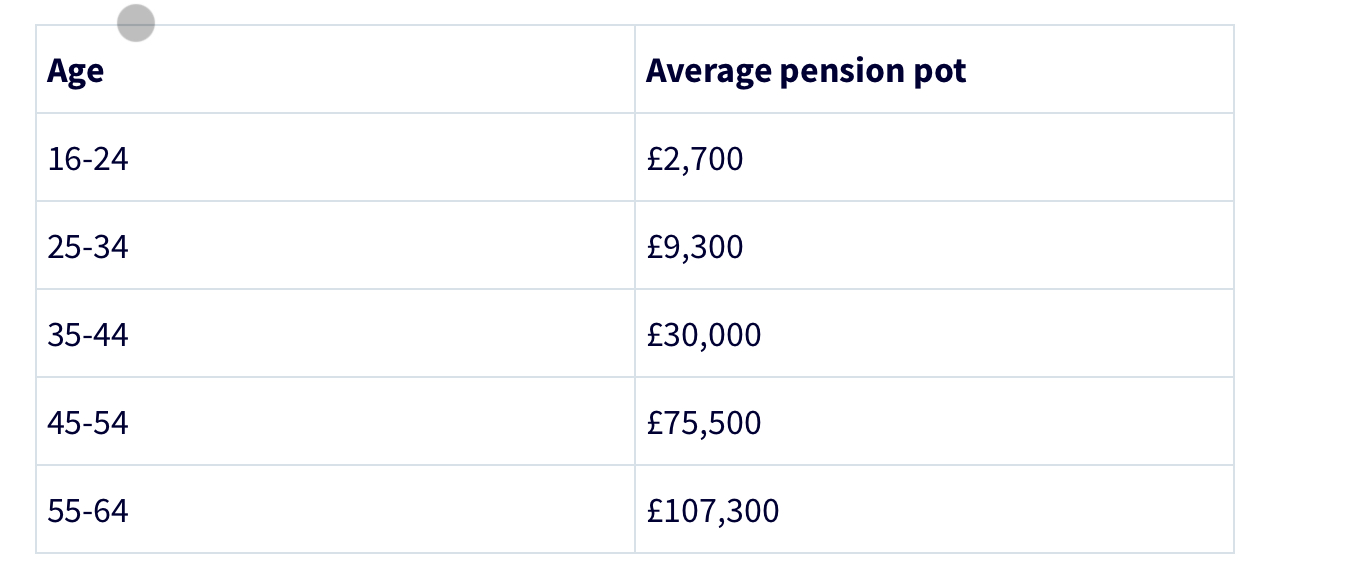

I pessimistically think the LTA abolishment will not last. The Conservative government’s day are currently numbered, and unless they can drastically change public opinion, it feels to me they’ll get the boot in the next election. If this happens and Labour wins, I can easily see some sort of LTA being reintroduced as it disproportionately benefits the wealthy. According to nutsaboutmoney, the average pension pot in the UK for people approaching retirement age is £107,000, nowhere near the LTA.

The increase in allowable pension contribution per tax year from £40,000 to £60,000 is valuable, especially for folk who want to bring their adjusted income down to < £240,000 and it should certainly be taken advantage of for those with slightly different FIRE goals than I. I pessimistically expect this to be reduced in the next parliament. It doesn’t stop you from benefiting from it for now though!

#3 I’m currently on track without changes!

You can see my post here about my plan to get to £2,000,000 invested and the main area of focus for me currently is actually building that pre-pension cash pot. I therefore will not be deferring tax and ensuring I max my ISA allowance and invest sensibly (read: boringly) in my GIA too.

Wrapping up

What initially sounded like an exciting change didn’t turn out to be as useful to me as I had hoped. However, it is still a net positive thing for the UK fat FIRE community and I’m sure others (perhaps those with larger income targets than I) will benefit from it.

When the government raise the ISA limit, you can expect to read a very excitable post from me about how it changes my thinking, but until then I’ll stick to my current plan and adapt it when policy changes again (which it certainly will).

I’d love to hear your thoughts on this so please leave them below!

the LTA being completely abolished was surprising indeed - great news if you are carting about a big DB pension (think in particular: high level civil servants) and looking to retire in the next couple of years...if you have just retired after planning for £1.1m, you'll be absolutely furious!

I suspected it would have been raised to e.g £1.5m or perhaps £2m which would have put it in line with what it was previously - £1.8m in 2011 - though still trailing an inflation adjusted figure (£2.4m IIRC)

still as you say: if you need the £££ before access age then that is that! other vehicles take priority as liquidity is needed

pensions still retain their exemption from estates (and by extension inheritance tax (IT)), so there is still scope for (now very) extensive generational planning assuming you do not need to draw down. you'll still get the charge at 75 ofc

or TL;DR: if you really want to 'win' on all counts - cram pension with millions, don't drawdown, die before 75, gg HMRC